The Social Security Administration oversees two programs, Social Security Disability Insurance and Supplemental Security Income, that pay monthly benefits to disabled individuals who qualify for them. Each program has other qualifying criteria, including sources of income, that you must meet in addition to being disabled to be eligible for benefits.

One of the most common challenges confronting applicants and people approved for benefits has to do with the types of income that must be reported to Social Security disability. Complicating matters are the different types of income and the fact that SSI and SSDI have different reporting requirements.

What follows should give you a better understanding of the rules for reporting types of income to SSD. Use it to familiarize yourself with the two programs as you prepare to meet with a Social Security disability lawyer at the Clauson Law Firm who will further assist you.

A look at the two disability programs administered by Social Security

SSI and SSDI are the two programs created by federal law to pay benefits to disabled individuals. The SSDI program is under Title II of the Social Security Act and pays benefits to individuals who worked long enough at jobs or through self-employment and paid Social Security taxes on their earnings and income to be "insured" under the program.

Some individuals without work history of their own may be eligible for SSDI benefits on the earnings history of a parent or spouse. For example, adults whose disability began before they were 22 years of age may be eligible for SSDI through the earnings record of a parent. If you have questions or need more information about SSDI benefits through the work record of a spouse or parent, speak with an SSD lawyer at the Clauson Law Firm.

The SSI program, which is contained in Title XVI of the Social Security Act, is a needs-based program paying benefits to disabled adults and children with limited income and resources who cannot afford to pay for such essential needs as food and shelter. SSI does not, as does the SSDI program, have a work component as part of its eligibility requirements.

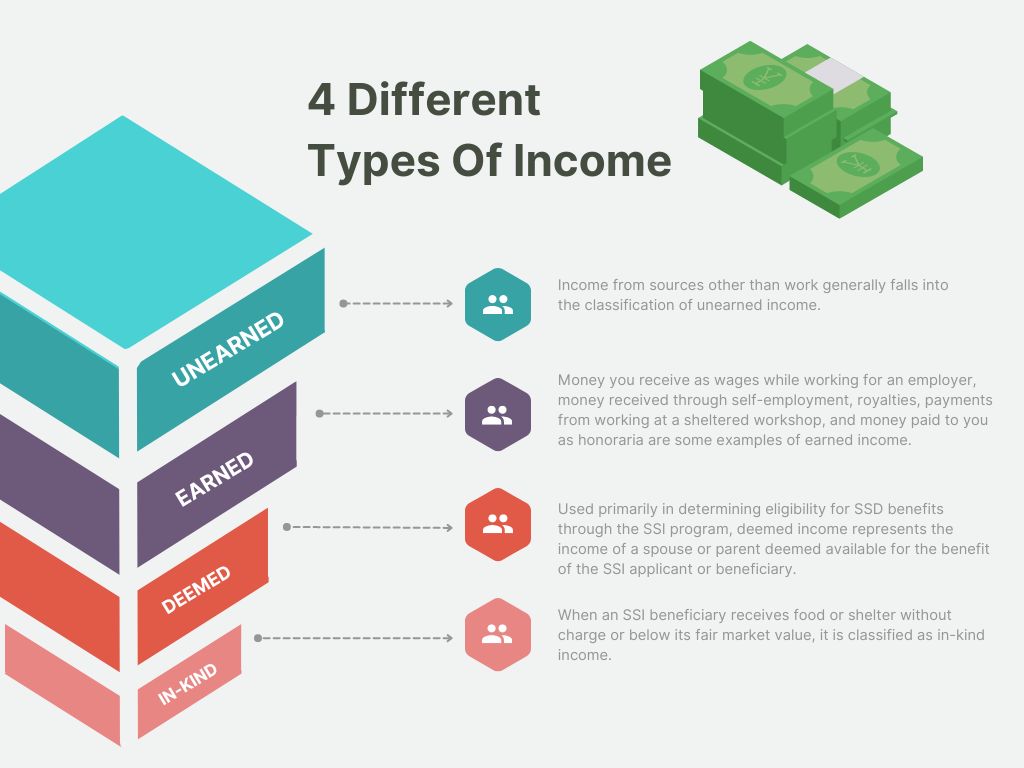

Four Different types of income

Social Security separates the types of income into four categories, but some of them may only apply to one and not both SSD benefits programs:

- Unearned income: Income from sources other than work generally falls into the classification of unearned income. Examples include Social Security benefits, pension benefits, payments from state-administered disability programs, money received from friends or relatives that you do not have to repay, unemployment benefits, dividends, and interest earned on investments.

- Earned income: Money you receive as wages while working for an employer, money received through self-employment, royalties, payments from working at a sheltered workshop, and money paid to you as honoraria are some examples of earned income.

- Deemed income: Used primarily in determining eligibility for SSD benefits through the SSI program, deemed income represents the income of a spouse or parent deemed available for the benefit of the SSI applicant or beneficiary.

- In-kind income: When an SSI beneficiary receives food or shelter without charge or below its fair market value, it is classified as in-kind income. An exception to the rule about in-kind income is when the food or shelter is provided by a nonprofit agency instead of a friend or relative of the beneficiary.

How Social Security applies the different types of income when considering an initial application for benefits or in determining ongoing eligibility for benefits depends on the SSD program.

Income and the SSI program

Your income from all sources cannot exceed the federal benefit rate to qualify for SSI benefits. The monthly federal benefit rate for 2021 is $794 for an individual and $1,191 for a couple. You can, however, have income that exceeds the federal benefit rate and still qualify for SSI or remain eligible to receive benefits if you have already been approved. The reason is that SSI does not consider all income sources as countable.

The following are only a few of the income exclusions that do not count against you when determining eligibility for SSI benefits:

- The first $20 a month of unearned income or, if you do not have unearned income in a given month, the exclusion may be applied toward earned income.

- The first $65 of monthly earned income.

- One-half of the remaining balance of earned income in a month after exclusion of the first $65.

- Income tax refunds.

- Supplemental Nutrition Assistance Program benefits, which are commonly known as food stamps or SNAP benefits.

- Grants or scholarships toward educational expenses and tuition.

- Money in the form of a loan that must be repaid.

It is essential that you speak with a disability lawyer at the Clauson Law Firm before making an income report to SSD because the list of income exclusions is quite lengthy. For example, an SSI beneficiary who is younger than 22 years of age and attending school may exclude as much as $1,930 a month in earnings from work up to a maximum of $7,770 per year. Those figures are for 2021 and may change in 2022, but a lawyer can determine whether or not you qualify for the exclusion.

If your countable income exceeds the federal benefit rate for SSI, you will not be eligible for benefits. Keep in mind that deemed income and in-kind income must be reported as types of income to SSD when applying for SSI. Any changes in deemed or in-kind income must be reported after you have been approved and are receiving benefits through SSI.

Reportable income under the SSDI program

To qualify for SSDI, you must have worked for a sufficiently long duration and contributed to the Social Security system by paying Social Security taxes on the income that you earned. Income does not factor into eligibility for benefits through SSDI as much as it does under the SSI program, but you still must report work income when receiving SSDI.

Reporting types of income to SSD generally focuses on wages from employment at a job and income earned through self-employment. If you earn more than $1,310 in a month in 2021, it shows that you can engage in substantial gainful activity and are no longer disabled. The monthly income limit for substantial gainful activity is $2,190 in 2021 for an individual who qualifies for benefits as being blind.

A physical or mental impairment that prevents you from engaging in substantial gainful activity is one of the factors used by Social Security to determine that a person is disabled and eligible for SSD benefits. The impairment or impairments must have lasted or be expected to last for at least 12 continuous months.

Other income sources that you must report under the SSDI program in addition to wages and self-employment income are the following:

- Sick pay.

- Vacation pay.

- State-administered disability payments.

- Workers' compensation benefits.

Unearned income, such as interest and dividends on investments, does not have to be reported because it does not factor into the eligibility process.

Trial work periods and reporting income

You should be mindful of the fact that Social Security encourages disabled individuals to test their ability to work without it affecting their SSD benefits through a trial work period. Money that you earn during the trial period, which is nine months though not necessarily consecutive as long as they are used within a 60-month period.

Any month that you earn more than $940 is a trial work period in 2021. The monthly amount increases to $970 in 2021. Even if you earn more than the substantial gainful activity limit during a trial work month, it will not affect the determination that you are disabled; nor will it reduce your monthly SSDI benefits.

When the trial work period is completed, a 36-month extended period of eligibility begins. During this extended period, earnings above the substantial gainful activity levels will be evaluated by the SSA to determine whether you continue to be disabled and eligible to receive SSDI benefits.

If the SSA determines that your earnings for a month exceed the income limits for substantial gainful activity it will treat your disability as ceased rather than terminated. Characterizing it as ceased allows SSA to pay for the month you exceed the limits and for an additional two months as a form of grace period.

Should your earnings during the grace period drop below the substantial gainful activity limits, your SSDI benefits may be reinstated without the need for filing a new application for benefits. Our SSD lawyer has more information about trial work periods and extended periods of eligibility.

Learn more about how to report income to SSD

An experienced disability lawyer at the Clauson Law Firm has answers to any question you have about SSD benefits, the application process, income reporting, and other issues that frequently arise with Social Security disability. Contact us today for more information and to arrange a free consultation.

Can I qualify for disability benefits without a work history of my own?

Some individuals not having a work history of their own may qualify for SSDI benefits based on the earnings history of a parent or spouse. It includes the case of an adult whose disability began before age 22 through the earnings record of a parent.

Does the money receive as a gift from my brother count toward my unearned income?

Yes, money received from friends or relatives that you are not supposed to repay counts towards your unearned income.